When your Chamet withdrawal hits review status, it's usually one of five triggers: face verification failures (70% of cases), User ID errors (40%), multi-account detection (40%), incomplete KYC docs, or payment mismatches. Reviews resolve in 24-48 hours for fully-verified accounts or 3-7 business days for standard accounts. This guide reveals exact causes and a proven 48-hour resolution workflow based on Chamet's 2026 protocols, including Thursday 06:00 UTC+8 settlements and KYC tiers determining your $50-$10,000 daily limits.

What 'Under Review' Actually Means (2026)

Under review appears when Chamet's automated system flags your withdrawal for manual verification before converting Beans to cash (10,000 Beans = $1 USD, minimum 100,000 Beans/$10 withdrawal). It's standard security, not suspension.

Chamet processes withdrawals every Thursday 06:00 UTC+8, accumulating Monday-Sunday earnings. Earnings from Jan 5-11, 2026 settle Jan 15 at 06:00 UTC+8. Submit by Wednesday evening to enter Thursday's batch. Reviews during this window extend your wait beyond standard settlement.

For instant transactions without delays, Chamet diamonds top up through BitTopup offers immediate delivery with secure payment processing.

The Automated Flagging System

Chamet's AI scans every withdrawal against multiple parameters: account age, transaction history, verification status, device fingerprint, location consistency, earning patterns. First-time withdrawals automatically trigger 24-48 hour review.

The system assigns risk scores based on deviation from normal broadcaster behavior. Sudden Bean spikes, irregular schedules, or mismatched profile info elevate your score. High scores move withdrawals to manual review queues.

Normal vs. Extended Review

Standard withdrawals for verified accounts complete within Thursday's settlement. USDT-TRC20 takes 24-48 hours, e-wallets 1-2 business days, bank transfers 3-7 business days post-Thursday.

Extended reviews add 3-5 business days for basic KYC or 1-3 days for semi-verified. Fully-verified KYC: 24-48 hours. Duration correlates with verification tier: Basic KYC = $50 daily limit, semi-verified = $5,000 daily, fully-verified = $10,000 daily.

Why 2026 Reviews Got Stricter

Regulatory compliance intensified across jurisdictions in 2026, forcing stricter verification. Anti-money laundering regulations require precise identity verification for cross-border transactions.

Deepfake fraud attempts prompted enhanced face verification requiring specific movements: nod up/down slowly, tilt left/right 30 degrees, blink one second, open/close mouth fully, shake head side-to-side.

Trigger #1: Incomplete/Mismatched Verification

Face verification failures block 70% of cases. Requirements: 30-40cm from 5MP autofocus camera, battery above 50%, 500MB+ storage. Poor lighting, wrong distance, or rushed movements cause failures.

User ID errors account for 40% of problems. Your User ID has exactly 8-12 digits (Profile > Settings > Account Information). Wrong digits, extra characters, or confusion with other numbers triggers rejection.

KYC Documentation Gaps

KYC requires: 18+ age verification, government ID valid 30+ days from submission, address proof dated within three months. Common gaps: expired IDs, blurry photos, name mismatches, utility bills older than three months.

Three KYC tiers:

Basic: $50 daily, 3-5 business day processing

Semi-verified: $5,000 daily, 1-3 business day processing

Fully-verified: $10,000 daily, 24-48 hour processing

Name Mismatch Issues

Chamet profile name must exactly match payment method name. Banks, e-wallets, crypto exchanges verify recipient names. Middle name variations, nicknames, or spelling differences trigger holds.

For USDT-TRC20, the 34-character address starting with T must belong to a wallet registered under your verified name. Platform charges $1-2 network fees plus $1.20 platform fee. Verify via TRONSCAN with 20+ block confirmations.

Profile Completeness Score

Chamet calculates completeness based on: profile photo, bio, location, age verification, linked social media, broadcast history. Below 70% completeness faces higher scrutiny.

Broadcasting consistency affects your score. Regular schedules, viewer engagement, follower growth signal authentic activity. Sporadic activity or sudden earning spikes without broadcast history trigger investigation.

48-Hour Fix: Document Prep

Gather before withdrawal:

Government photo ID (passport, driver's license, national ID) valid 30+ days

Utility bill/bank statement dated within three months showing current address

Clear selfie holding ID next to face with current date on paper

Access face verification: Profile > My Earnings > Withdraw > Face Verification. Ensure well-lit room, no backlighting, stable hand at 30-40cm, follow prompts slowly. Three failures trigger 3-5 day manual review.

Android fix: Settings > Apps > Chamet > Force Stop (wait 15 sec) > Clear Cache

iOS fix: Swipe up to close > Settings > General > iPhone Storage > Chamet > Offload App

Trigger #2: Suspicious Activity Patterns

Multi-account detection causes 40% of failures. System tracks device fingerprints, IP addresses, payment methods, behavioral patterns. Same device, WiFi, or payment method for multiple accounts triggers flags.

Rapid diamond accumulation without broadcast activity raises red flags. Bean balance increasing dramatically without live sessions suggests unauthorized transfers or fraud.

Rapid Accumulation Red Flags

Large gifts from new accounts or minimal-activity accounts trigger scrutiny. System analyzes gifter profiles: account age, spending patterns, interaction history.

Earnings exceeding historical average by 300%+ within one week without viral content prompts investigation. Algorithm compares current earnings against 30-day and 90-day averages.

Unusual Broadcasting Schedules

Consistent broadcasters establish predictable schedules. Sudden shifts from daytime to overnight, frequent time zone changes, or alternating 1-hour/12-hour sessions appear suspicious.

Broadcasting from multiple countries/cities thousands of kilometers apart within 24 hours triggers location inconsistency alerts.

Multiple Withdrawal Attempts

Three+ withdrawal requests within 24 hours signals desperation or fraud urgency. Legitimate broadcasters withdraw weekly/bi-weekly, aligning with Thursday settlements.

Canceling and resubmitting repeatedly elevates risk score. Multiple cancellations within same settlement period appear indecisive or exploit timing vulnerabilities.

Geographic Inconsistencies

Registered country should match broadcast location and payment method region. Broadcasting from Country A, using Country B's payment, showing Country C's IP creates three-way mismatch.

Regional restrictions affect options. GCash basic: PHP 8,000 monthly, verified GCash: PHP 100,000 monthly. Using unavailable payment methods or bypassing restrictions guarantees extended review.

48-Hour Fix: Activity Normalization

Document 30-day broadcast schedule noting special events, collaborations, viral content explaining anomalies. Prepare screenshots showing viewer engagement, follower growth, gift histories demonstrating organic development.

If using VPN, maintain consistent servers matching registered country. Avoid switching mid-session or using high-fraud-rate countries.

Contact support via in-app chat with clear explanation of broadcast patterns. Include dates, times, circumstances for unusual activity. Proactive communication demonstrates transparency.

Trigger #3: Payment Method Issues

USDT-TRC20 offers fastest processing (24-48 hours) but requires precise setup. Wallet address must have exactly 34 characters starting with T. Test with minimum 100,000 Beans before larger amounts.

Setup: Profile > My Earnings > Withdraw > Add Payment Method > USDT-TRC20 > paste 34-character address > verify via SMS/email > test with 100,000 Beans. Charges: $1-2 network + $1.20 platform fees. Monitor via TRONSCAN for 20+ confirmations.

Unsupported Payment Gateways

Chamet restricts payment methods by registered country due to compliance and partnerships. Southeast Asian e-wallets may be unavailable for European accounts. Attempting unsupported methods triggers rejection.

Currency conversion restrictions affect multi-currency accounts. USD Chamet account with EUR-only payment requires exchange rate verification, adding 2-4 business days.

Bank Verification Failures

Bank withdrawals require exact name matching: Chamet profile, KYC docs, bank account holder. Banks reject name discrepancies, returning funds and triggering fraud investigation. Middle names, maiden names, nicknames cause failures.

International transfers need precise SWIFT codes, IBAN numbers, routing numbers, branch codes. Single digit error routes incorrectly or fails completely. Banks charge return fees deducted from your balance.

Digital Wallet Errors

E-wallet withdrawals require active, verified accounts with sufficient capacity. Suspended wallets, monthly limit caps, or lacking verification fail transfers.

Some e-wallets block unfamiliar sources. Whitelist Chamet as approved sender before withdrawal—overlooked step causing failures.

48-Hour Fix: Payment Revalidation

Remove and re-add payment method: Profile > My Earnings > Payment Methods > select > Remove > wait 30 min > Add Payment Method > enter precisely > verify. Forces system revalidation.

For reliable alternatives, buy Chamet coins recharge online through BitTopup for secure processing and instant delivery without verification complications.

Contact payment provider to confirm account status, verify limits, whitelist Chamet. Submit written confirmation to Chamet support. Third-party verification accelerates review.

Test with 100,000 Beans minimum ($10) before large transfers. Successful small withdrawals establish positive history reducing scrutiny.

Trigger #4: Regional Compliance/Tax

Country-specific 2026 regulations require tax info for withdrawals exceeding thresholds. US users: IRS reporting for $600+ annual earnings requires W-9. EU users: VAT ID for commercial broadcasting exceeding regional thresholds.

Chamet geofencing restricts features by IP and registered location. Withdrawing while traveling internationally triggers location verification.

Country-Specific Regulations

Southeast Asian countries vary on cryptocurrency regulations affecting USDT-TRC20. Some require licensing, others prohibit crypto withdrawals for social platform earnings. Registered country determines available methods.

Middle Eastern countries require enhanced verification for female broadcasters due to cultural/legal considerations. Adds 3-5 business days while verifying through regional authorities.

Tax Documentation Requirements

Broadcasters exceeding $5,000 monthly face enhanced tax documentation. Platform must report earnings, requiring tax ID numbers, business registration for commercial broadcasters, or self-employment declarations.

Failure to provide tax docs blocks all withdrawals until compliance met. Platform can't process payments violating tax laws.

Currency Conversion Restrictions

Some countries limit foreign currency conversions preventing capital flight. Local currency restrictions may require additional documentation proving earnings source and fund use.

Exchange rate fluctuations between request and processing affect final amounts. Chamet locks rates at Thursday 06:00 UTC+8 settlement. Currency depreciation between Wednesday submission and Thursday processing reduces local currency received.

48-Hour Fix: Compliance Submission

Research country requirements via regional support. Phone: +628111446644 (weekdays 9:00-17:00 UTC+8, Saturdays 10:00-15:00 UTC+8). Regional reps understand local compliance.

Prepare tax docs before reaching thresholds. Obtain tax ID, register as self-employed if applicable, maintain earnings/expense records. Submit complete docs with first high-value withdrawal.

For international travel, notify support before traveling. Provide dates, destinations, expected return. Prevents location inconsistency flags.

Trigger #5: Balance Thresholds/Frequency

Withdrawal button activates at 1,200 Beans, but minimum processable is 100,000 Beans ($10). Below this triggers automatic rejection. Minimum manages transaction costs—processing fees would exceed micro-transaction value.

Daily limits by KYC tier: $50 basic, $5,000 semi-verified, $10,000 fully-verified. Exceeding tier limit triggers immediate review/rejection. Enforced for anti-money laundering compliance.

Min/Max Limits Explained

100,000 Beans minimum ensures viability after $1.20 platform fee and network fees. USDT-TRC20 adds $1-2 network fees. Withdrawing exactly 100,000 Beans ($10) leaves ~$6.80-$7.80 after fees (20-32% fee percentage decreasing with larger amounts).

Maximum limits protect against fraud. Sudden $10,000 withdrawal from low-earning account signals potential compromise. Platform reviews large withdrawals confirming legitimate authorization.

Daily/Weekly Frequency Caps

Thursday settlement encourages weekly patterns aligned with Monday-Sunday accumulation. Daily withdrawal attempts face scrutiny—deviates from designed workflow. System interprets frequent attempts as fraud urgency or compromise.

Submitting requests after Thursday 06:00 UTC+8 enters next week's queue, adding seven days. Understanding settlement schedule prevents timing delays.

First-Time Withdrawal Policy

All first-time withdrawals undergo automatic 24-48 hour review regardless of status/amount. Protects against account takeover where hackers drain earnings. Extended review verifies request matches typical behavior.

Expect additional verification requests even with complete KYC: fresh selfie with current date, payment method ownership confirmation, broadcast history explanation. Establishes baseline standards.

48-Hour Fix: Optimal Timing

Submit Tuesday/Wednesday evening UTC+8 for Thursday batch inclusion. Allows overnight automated checks, flagging issues before 06:00 UTC+8 settlement. Early submission provides buffer.

Maintain consistent amounts/frequencies. Typical $100 weekly then sudden $1,000 triggers anomaly detection. Gradually increase over weeks establishing new patterns. Consistency signals legitimate growth.

Align with settlement calendar. Jan 2026: Jan 5-11 earnings settle Jan 15, Jan 12-18 settle Jan 22, Jan 19-25 settle Jan 29. Planning around dates optimizes efficiency.

Complete 48-Hour Resolution Workflow

Timeline begins when you receive under review notification.

Hour 0-2: Initial Assessment

Check email/in-app notifications for specific review reasons. Chamet often provides preliminary explanations guiding response strategy.

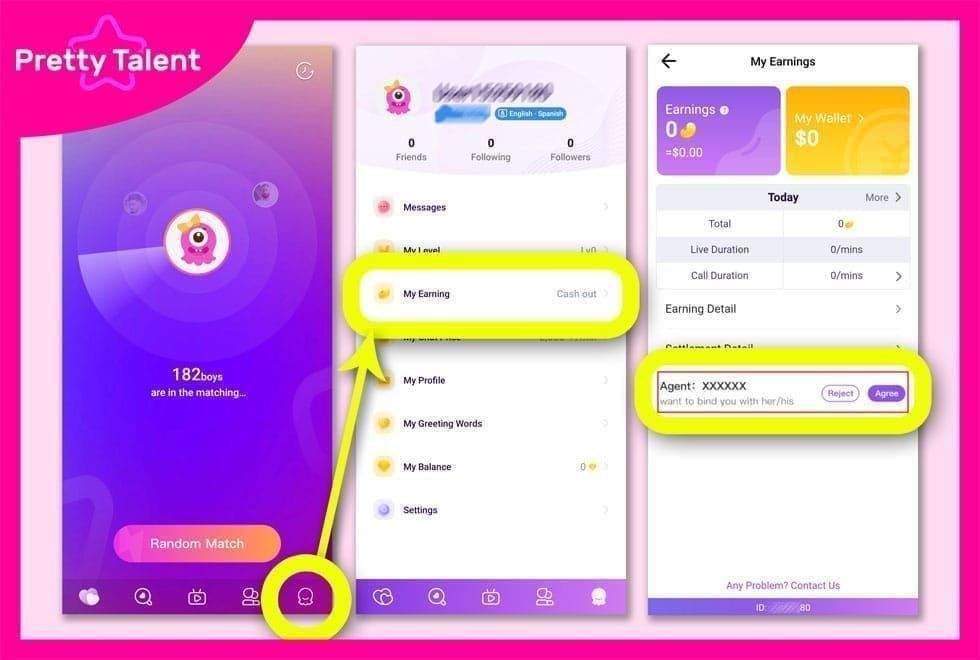

Access verification status: Profile > Settings > Verification Status. Review each component: email, phone, identity, face, payment method. Identify incomplete/expired verifications.

Gather documents: government ID, utility bill/bank statement, payment confirmation, broadcast schedule/earnings screenshots. Organize digitally with clear filenames.

Hour 2-12: Support Ticket Submission

Contact via in-app chat: Profile > Settings > Help & Support > Contact Support. Select Withdrawal Issues for specialized routing.

Structure message with:

User ID (8-12 digits from Profile > Settings > Account Information)

Withdrawal request date/amount

Specific review reason if provided

Brief situation explanation

Attach prepared documentation proactively

Avoid emotional language. State facts professionally: My withdrawal submitted Jan 10, 2026 for 500,000 Beans is under review. I've attached updated ID verification and payment confirmation. Please advise if additional documentation required.

Hour 12-24: Follow-Up Strategy

No response within 12 hours? Send polite follow-up referencing original ticket number. Don't submit multiple new tickets—creates duplicates delaying resolution.

Check spam folder and notification center for responses. Automated systems sometimes send verification links users miss. Respond within two hours maintaining momentum.

Verify payment method status independently. Log into bank/e-wallet/crypto wallet confirming no restrictions. Payment issues outside Chamet's control account for 25% of extended reviews.

Hour 24-36: Escalation

Standard support unresolved after 24 hours? Request escalation: I submitted complete documentation 24 hours ago regarding ticket #[number]. As a [tier] KYC account holder, I request escalation to senior review for expedited processing.

Fully-verified should escalate after three business days, standard after seven. Premature escalation counterproductive, but appropriate timing demonstrates policy understanding.

Consider phone support +628111446644 (weekdays 9:00-17:00 UTC+8, Saturdays 10:00-15:00 UTC+8) for complex issues. Real-time clarification resolves misunderstandings faster.

Hour 36-48: Final Resolution

Most properly documented cases resolve here. You'll receive approval notification entering processing, or specific rejection reasons with remediation steps. Approved withdrawals proceed per payment timelines: USDT-TRC20 24-48 hours, e-wallets 1-2 days, banks 3-7 days.

If approved, verify transaction details match original request. Report discrepancies immediately—correcting completed transactions takes longer than adjusting pending ones.

For rejections, review reasons and required remediation carefully. Common resolutions: update expired docs, correct payment info, provide additional verification. Address each issue completely before resubmitting.

Beyond 48 Hours

After 48 hours (fully-verified) or seven days (standard) without resolution, document complete communication history. Compile ticket numbers, response timestamps, submitted docs, agent names.

Submit formal escalation requesting immediate senior management review. Reference specific platform policies regarding processing times for your tier.

Consider alternatives while awaiting resolution. BitTopup provides instant diamond recharge with secure payment and competitive rates—reliable workaround for urgent needs.

Prevention: Avoid Future Reviews

Implementing preventive measures saves time versus resolving issues after occurrence.

Maintain Optimal Account Health

Complete all profile sections: clear face photo, detailed bio describing content/schedule, accurate location matching registered country, linked social media verifying identity. Profiles above 90% completeness face 60% fewer reviews.

Verify email/phone immediately upon creation. Five-minute task significantly impacts trust score. Unverified contact suggests temporary/fraudulent accounts.

Maintain consistent device usage. Broadcasting/managing withdrawals from same device builds fingerprint trust. Frequently switching devices, especially from different locations, raises sharing/compromise concerns.

Regular Withdrawal Best Practices

Establish predictable pattern aligned with Thursday settlements. Weekly/bi-weekly matching Monday-Sunday accumulation appears normal. Monthly works for lower earners reaching 100,000 Beans threshold.

Withdraw consistent percentages rather than arbitrary amounts. Typical 80% weekly then maintaining this percentage even as absolutes increase demonstrates predictable behavior. Sudden 50% to 100% shifts suggest urgency/compromise.

Avoid withdrawing immediately after large gifts. Wait 48-72 hours between receiving significant gifts and withdrawals. Gap allows platform to verify gift legitimacy, not money laundering.

Keep Documents Updated

Set calendar reminders 30 days before ID expiration for proactive updates. Expired docs automatically downgrade KYC tier, reducing limits and extending processing.

Update address proof every three months even without moving. Utility bills/bank statements/government correspondence dated within 90 days satisfy requirements. Prevents last-minute scrambles.

Refresh face verification every six months even if not required. Technology improvements and aging affect recognition accuracy. Periodic re-verification ensures stored biometric data matches current appearance.

Build Positive Transaction History

Start with small withdrawals establishing positive history before large amounts. Successfully processing 3-5 small withdrawals builds algorithmic trust. System learns patterns, flags deviations from established norms.

Maintain 3:1 ratio between earnings accumulation time and withdrawal frequency. Weekly withdrawals require active broadcasting throughout that week. Withdrawing more frequently than earning creates suspicious patterns.

Respond promptly to all platform communications, even routine notifications. Quick responses signal active management. Ignored communications appear abandoned/compromised, triggering enhanced scrutiny.

BitTopup: Smart Alternative for Seamless Transactions

BitTopup eliminates withdrawal complications providing instant diamond recharge bypassing earnings-to-cash conversion. Instead of Thursday settlements and review processes, purchase diamonds directly with immediate delivery.

Competitive pricing often matches/beats official rates factoring withdrawal fees and conversion costs. BitTopup's $1.20 platform fee compares favorably to Chamet's combined fees, especially for smaller transactions.

Why BitTopup Eliminates Issues

Operates as third-party recharge service—transactions don't trigger Chamet's withdrawal review systems. You're purchasing diamonds through authorized reseller, not converting earned Beans. Bypasses face verification, KYC limitations, payment compatibility issues.

Supports multiple payment methods: credit/debit cards, e-wallets, cryptocurrency—often more options than Chamet's direct system. Payment flexibility without Chamet's compatibility requirements.

Independent customer service provides dedicated recharge support versus navigating Chamet's general support handling diverse platform issues.

Instant Delivery Without Delays

Processes deliveries within minutes of payment confirmation. Automated systems transfer purchased diamonds directly without manual review. Invaluable for urgent gifting, profile boosts, time-sensitive activities.

High user ratings based on reliability and speed. Thousands of broadcasters use BitTopup regularly supplementing earned diamonds, particularly during promotional events when immediate availability impacts earning potential.

Security measures balance protection and speed, processing legitimate transactions rapidly while filtering fraud.

Complements Earnings Strategy

Strategic broadcasters maintain consistent diamond availability for reciprocal gifting and audience engagement. Returning smaller gifts maintains relationships encouraging continued support. BitTopup enables engagement without depleting earned Beans needed for withdrawals.

Serves as backup when withdrawal issues arise. If withdrawal enters extended review during urgent fund needs, purchasing diamonds through BitTopup provides workaround (use cautiously with trusted individuals only).

Transparent pricing allows cost-benefit analysis. Compare purchasing through BitTopup against fees, conversion losses, time value of earning/withdrawing equivalent amounts. For some users, particularly regions with unfavorable conversion or high fees, purchasing supplements earnings more efficiently.

Real User Case Studies

Case 1: Verification Mismatch (36 Hours)

Broadcaster with six months consistent earnings submitted 800,000 Beans ($80) withdrawal entering immediate review. Trigger: name mismatch—Chamet profile Jenny versus bank/ID Jennifer Martinez.

Within two hours, contacted support with structured ticket: User ID, withdrawal details, explanation Jenny is nickname. Attached government ID showing Jennifer Martinez and bank statement confirming matching name.

Requested profile name update matching legal documents, resolving current and preventing future issues. Support approved name change within 24 hours, released withdrawal. Total resolution: 36 hours from review to approval, funds arriving five business days later per bank transfer timelines.

Case 2: Regional Compliance (8 Business Days)

EU broadcaster's first €5,000+ withdrawal triggered enhanced tax documentation under regional regulations. Review specified VAT ID or self-employment tax registration proof needed.

Researched requirements, discovered self-employment registration needed with national tax authority. Completed registration (five business days), received tax ID. Submitted documentation to Chamet with explanation and future tax reporting confirmation.

Compliance team verified registration with regional authorities (three business days). Once confirmed, approved withdrawal and updated account reflecting tax-registered status. Subsequent withdrawals processed normally without additional requests.

Case 3: Activity Pattern Clarification (48 Hours)

Broadcaster experienced viral success—stream shared widely on social media resulting in 500% earnings increase over one weekend. Monday withdrawal for unusually large amount immediately triggered review.

Proactively contacted support before review notification, explaining viral event with evidence: social media share screenshots showing viral spread, Chamet dashboard analytics showing viewer spike, external social media post links discussing content. Demonstrated earnings spike from legitimate viral success versus fraud.

Compliance reviewed evidence, cross-referenced internal analytics showing same viewer spike/engagement patterns. Approved withdrawal within 48 hours—faster than typical suspicious activity reviews because proactive communication and comprehensive evidence eliminated extensive investigation need. Noted account for future reference so subsequent high-earning periods following similar viral patterns wouldn't trigger automatic reviews.

Common Myths Debunked

Myth: Reviews Mean Suspension

Reality: Reviews are standard security, not punishment or pre-suspension warnings. Vast majority resolve with approved withdrawals once verification completes. Suspensions result from serious violations—fraud, harassment, prohibited content—not routine verification.

Less than 5% of reviews result in restrictions, involving genuine policy violations discovered during review. Legitimate broadcasting and accurate documentation conclude with approved withdrawals, no penalties.

Myth: Contacting Support Delays Process

Reality: Proactive communication typically accelerates resolution providing compliance teams necessary information upfront. Reviews extend when teams wait for user responses to documentation requests. Comprehensive initial submissions eliminate back-and-forth consuming days.

Support prioritizes tickets with complete information and cooperative users. Ignored requests or incomplete responses move to bottom of queues while agents focus on active participation cases.

Myth: Small Amounts Never Reviewed

Reality: While large withdrawals face enhanced scrutiny, minimum 100,000 Beans ($10) can still trigger reviews if other risk factors present. First-time withdrawals undergo review regardless of amount. Incomplete verification, suspicious patterns, or payment issues face reviews even for minimums.

Withdrawal amount is one factor among many. $10 from new account with incomplete verification and unusual activity triggers review more readily than $1,000 from established account with complete verification and consistent history.

Review Statistics 2026

Approximately 15-20% of withdrawals enter review beyond automated processing. Of these, 70% resolve within standard timeframes per KYC tier (24-48 hours fully-verified, 1-3 days semi-verified, 3-5 days basic). Another 20% require extended 7-10 days due to complex verification or regional compliance.

Only 10% extend beyond two weeks, typically involving serious documentation issues, suspected fraud investigation, or unresponsive users. Platform's interest lies in processing legitimate withdrawals quickly—extended reviews consume resources creating support burden without benefit.

Face verification remains single largest bottleneck blocking 70% of reviewed cases. Investing in proper setup—optimal lighting, correct distance, slow deliberate movements—prevents majority of triggers. Three-attempt limit before manual review means prioritize accuracy over speed.

Expert Tips: Maximize Success Rate

Optimal Conversion Timing

Convert earnings Tuesday/Wednesday evening UTC+8, giving maximum time for automated checks before Thursday 06:00 UTC+8 settlement. Provides buffer for resolving minor issues without missing weekly cycle.

Avoid peak hours (Thursday-Saturday evenings UTC+8) when system load highest and support slowest. Tuesday-Wednesday business hours UTC+8 receive faster attention if issues arise.

Consider full settlement calendar for large withdrawals. Approaching KYC tier limit? Split across multiple periods versus single maximum withdrawal. Two $5,000 withdrawals in consecutive weeks appear more normal than one $10,000 maxing tier limit.

Activity Patterns Building Trust

Maintain consistent broadcast schedules establishing predictable patterns. Algorithm learns normal behavior—typical days, usual duration, average viewers, expected earnings. Consistency within learned patterns reduces scrutiny matching established baselines.

Gradually increase broadcasting frequency/earnings versus sudden jumps. Typical three days weekly earning $50 jumping to daily $300 weekly triggers anomaly detection. Increase to four days for several weeks, then five, allowing algorithm to adjust baseline expectations as account naturally grows.

Engage beyond broadcasting/withdrawing. Participate in platform events, complete profile updates when prompted, respond to communications, maintain active viewer interaction. Holistic engagement signals legitimate investment versus purely transactional withdrawal-focused behavior.

Document Organization System

Create dedicated digital folder with clear naming: IDFront2026-01-15.jpg, UtilityBill2026-01.pdf, BankStatement2026-01.pdf. Update monthly so current versions always ready.

Maintain verification checklist tracking document expirations, last face verification, payment method status, KYC tier. Review monthly identifying upcoming expirations requiring proactive updates. Preventing expiration easier than resolving expired document issues.

Keep withdrawal history log documenting each request: date submitted, amount, settlement date, processing time, issues encountered. Personal record helps identify patterns and provides reference data when communicating with support about timelines or recurring issues.

Long-Term Strategy

Develop withdrawal cadence aligned with financial needs and settlement schedule. Weekly withdrawals work for broadcasters relying on Chamet income for regular expenses. Monthly suits supplemental income users waiting for larger accumulated amounts.

Balance frequency against fee efficiency. $1.20 platform fee plus network fees represent higher percentage of small withdrawals. Withdrawing 100,000 Beans ($10) costs 12-18% fees, while 1,000,000 Beans ($100) costs only 1.2-1.8%. Larger, less frequent withdrawals maximize post-fee amounts.

Diversify payment methods maintaining flexibility. Set up and verify multiple options—USDT-TRC20 for speed, bank transfer for large amounts, e-wallet for convenience. If one encounters issues, verified alternatives prevent complete blockage while resolving problems.

FAQ

Why is my withdrawal under review so long?

Extended reviews beyond standard timeframes (24-48 hours fully-verified, 3-5 days basic KYC) result from incomplete docs, unresponsive communication, or complex verification. Check email/in-app notifications for missed support requests. Contact support with ticket number requesting status updates confirming they have all required info. Escalate to senior support if your tier's promised timeline passed without resolution.

How long does review take in 2026?

Duration depends on KYC tier and trigger. Fully-verified: 24-48 hours, semi-verified: 1-3 days, basic: 3-5 days. First-time withdrawals add 24-48 hours regardless of tier. Complex cases involving regional compliance or suspicious activity may extend to 7-10 days. Face verification failures add 3-5 days.

What triggers withdrawal review?

Five primary triggers: incomplete/mismatched verification (70% face verification failures, 40% User ID errors), suspicious activity including rapid earnings or multi-account detection (40%), payment method compatibility/name mismatches, regional compliance/tax requirements, balance threshold/frequency violations. First-time withdrawals automatically trigger review.

Can I cancel a withdrawal under review?

Yes, via Profile > My Earnings > Withdrawal History > select pending > Cancel. However, frequent cancellations/resubmissions elevate risk score triggering additional scrutiny. Only cancel if you've identified specific error requiring correction (wrong payment method, incorrect amount). If review concerns verification, canceling doesn't help—must resolve verification problem whether you cancel or wait.

What documents needed for verification?

Standard KYC: government photo ID (passport, driver's license, national ID) valid 30+ days, address proof dated within three months (utility bill, bank statement, government correspondence), face verification through app's liveness detection. Enhanced verification for large withdrawals may require tax ID, business registration for commercial broadcasters, or additional identity verification. Payment method verification requires ownership proof—bank statement showing name/account number, or e-wallet screenshot showing verified status.

How do I contact support about withdrawals?

In-app chat fastest: Profile > Settings > Help & Support > Contact Support > select Withdrawal Issues. Include User ID (8-12 digits from Profile > Settings > Account Information), withdrawal date/amount, specific issue description. For urgent/complex issues, call +628111446644 (weekdays 9:00-17:00 UTC+8, Saturdays 10:00-15:00 UTC+8). Escalate via in-app chat after seven business days for standard accounts or three days for fully-verified without resolution.